EUR/USD: Rate Drops, Dollar Falls

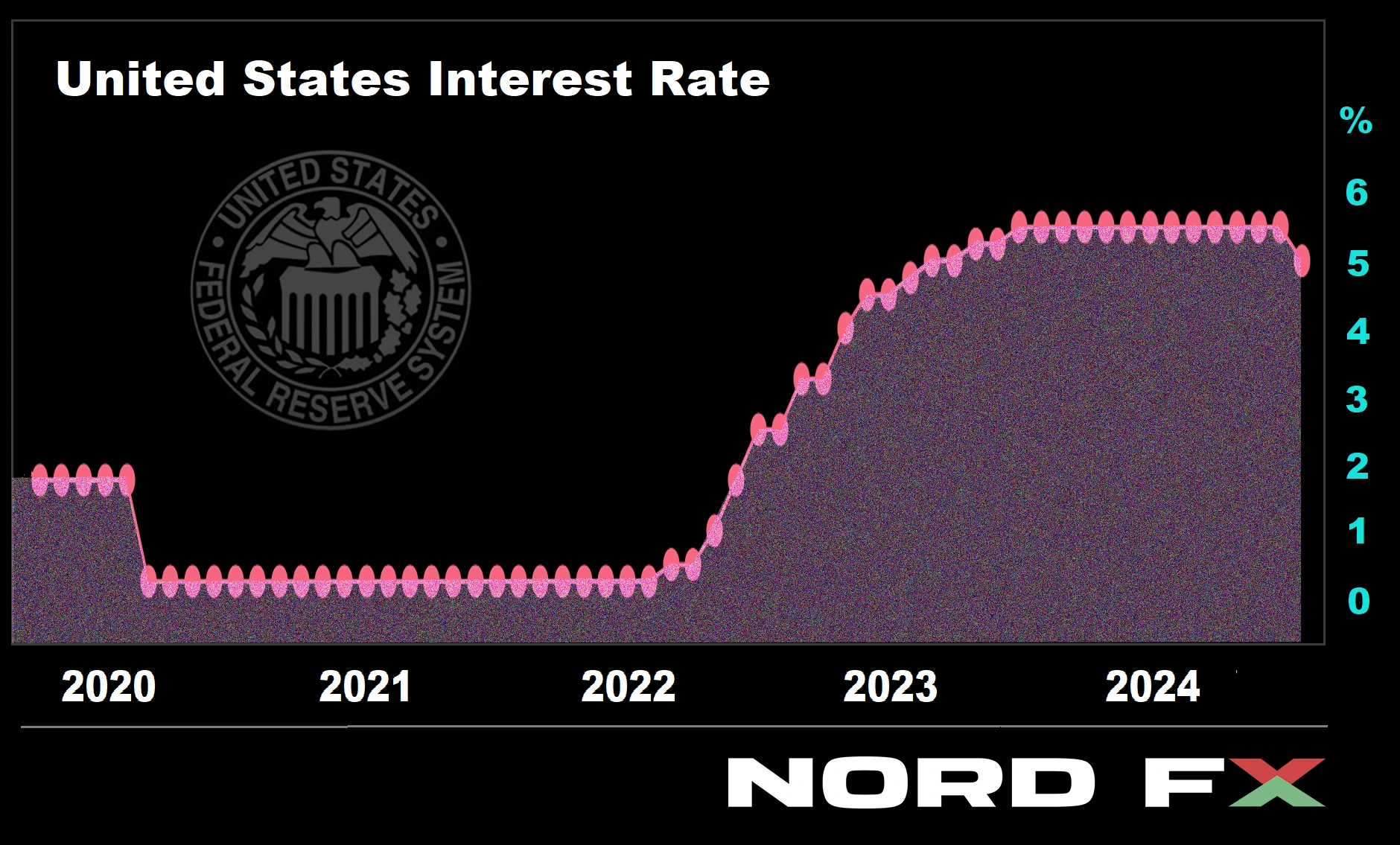

● The United States Federal Reserve System (Fed) announced its decision on the benchmark interest rate following the two-day meeting held on September 17-18. The intrigue lay in the rate cut step—whether it would be the standard 25 basis points (bps) or twice as much. On the eve of the meeting, according to market expectations, the probability of a 25 bps decrease was 45%, and a 50 bps decrease was 55%. As a result, for the first time in four years, the regulator opted to reduce the rate by half a percent immediately: from the highest in 23 years of 5.50% to 5.00%.

● It should be noted that at the beginning of the easing of monetary policy (QE), such a large rate cut was applied by the Federal Reserve relatively rarely and only in critical situations. For example, in this century, this occurred in 2001 (following the attack on the World Trade Center in New York), in 2007 (the onset of the economic crisis), and in 2020 (the COVID-19 pandemic). However, such a force majeure event is not currently observed, so why did the American central bank take this step?

Several analysts explain this by stating that the Fed was delayed in lowering the rate in July and is now striving to catch up. (Recall that several members of the FOMC [Federal Open Market Committee] were ready to start cutting rates as early as mid-summer.) Fed Chair Jerome Powell did not agree with the version of a delay. On the other hand, he acknowledged that if the labor market data in July had been released before rather than after the FOMC meeting, the decision could have been different.

The current September meeting was also notable because, for the first time since 2005, the Fed's decision was not unanimous. One of the 12 FOMC members, Michelle Bowman, publicly advocated for a 25 bps rate cut instead of 50 bps.

● The Fed's updated macroeconomic forecasts, following the September 17-18 meeting, suggest a faster decline in inflation and higher unemployment rates. Jerome Powell referred to this as a shift in the balance of risks.

According to the new forecast, inflation (PCE index) this year will be 2.3% (June forecast was 2.6%), next year – 2.1% (June was 2.3%), and finally in 2026, inflation will decrease to the target of 2.0% (unchanged). In 2027 and beyond, inflation rates will remain at the target level.

As for the unemployment forecast in the United States, it has been raised for 2024 from 4.0% to 4.4%, in 2025 it is expected to remain at 4.4% (June was 4.2%), and in 2026 to decrease to 4.3% (June was 4.1%). The Fed expects that starting in 2027 and onward, unemployment will hold steady at 4.2%.

The forecast for US GDP growth in 2024 has been lowered from 2.1% to 2.0%, with the same figure planned for 2025-2027, which is overall above the long-term trend of 1.8%.

● The regulator also announced that interest rate cuts will continue. However, due to changes in inflation and labor market forecasts, the rate outlook has been significantly softened. Thus, the Fed plans to see the rate at 4.5% by the end of the year (i.e., possibly two more cuts: in November and December by 25 bps each). In the one-year perspective, the rate is expected to be 3.4%, and then 2.9%.

It is important to understand that these are only forecasts, which can (and will) change depending on the geopolitical situation in the world and the internal situation in the United States. For example, experts expect a serious increase in the budget deficit in the event of Donald Trump coming to the White House. This could seriously slow the pace of QE.

● Regarding the euro, the pan-European currency has recently been supported by statements from high-ranking EU officials. For example, ECB Vice-President Luis de Guindos stated last week that “we have left the door completely open, […] and in December we will have more information than in October.” These words are an obvious hint that the regulator does not intend to make any rate decisions before December. ECB Governing Council member and Governor of the Bank of Lithuania, Gediminas Šimkus, also tempered market expectations by stating on Tuesday, September 17, that “the probability of a rate cut in October is very low.” “In October, we will not have much new data. And the economy is developing according to forecasts,” he added.

Currently, the ECB's key interest rate stands at 3.65%. Thus, if the difference between the Fed's and the ECB's (and other central banks') interest rates narrows by the end of this year and throughout the next year, it will put pressure on the dollar. Meanwhile, the market reaction to the Fed's September decision was quite subdued. Of course, forecasts for further rate cuts helped risk assets. The stock indices S&P 500, Dow Jones, and Nasdaq continued to rise, and leading cryptocurrencies improved their positions. Conversely, the Dollar Index (DXY) fell. The EUR/USD pair, being inversely correlated with it, first rose to 1.1188, then fell to 1.1080, showing maximum weekly volatility of 108 points. Then the fluctuations began to diminish, the waves gradually subsided, and the pair ended the workweek at 1.1162.

● Expert opinions regarding EUR/USD's behaviour in the near term are divided as follows: only 20% of analysts voted for a strengthening dollar and a decline in the pair, 65% for its growth, and another 15% took a neutral position. However, when moving to a medium-term forecast, the picture changes sharply. Here, 65% are on the side of the US currency, predicting the pair to fall below 1.1000. Supporters of the euro in this time horizon are only 20%, while 15% still remain neutral, refusing to make forecasts. In technical analysis on the D1 chart, all 100% of trend indicators and oscillators are colored green, although a quarter of the latter are signalling overbought conditions. The nearest support for the pair is located in the zone 1.1135-1.1150, then 1.1100, 1.1000-1.1025, 1.0880-1.0910, 1.0780-1.0805, 1.0725, 1.0665-1.0680, 1.0600-1.0620. Resistance zones are in the regions of 1.1185-1.1200, 1.1275, 1.1385, 1.1485-1.1505, 1.1670-1.1690, and 1.1875-1.1905.

● This upcoming week, the dynamics of major dollar pairs EUR/USD, GBP/USD, and USD/JPY may be significantly influenced by the following events. On Monday, September 23, preliminary Purchasing Managers' Index (PMI) data will be released for various sectors of the economies of Germany, the Eurozone, the United Kingdom, and the United States. Following a brief pause in the flow of important economic news, on Thursday, September 26, the US GDP data for the second quarter and the number of initial jobless claims in the country will be published. Additionally, scheduled for this day are the hearing of the inflation report in the UK Parliament and a speech by Federal Reserve Chair Jerome Powell. At the very end of the workweek, on Friday, September 27, inflation data for the Tokyo region (Japan) will be released. Moreover, on this day, we will receive another set of inflation statistics from the United States in the form of the Core Personal Consumption Expenditures (PCE) Price Index. Traders dealing with yen pairs should also note that Monday, September 23, is a holiday in Japan, as the country observes the Autumnal Equinox Day.

GBP/USD: Rate Unchanged, Pound Rises

● Last week, two more central bank meetings took place: the Bank of England (BoE) on Thursday, September 19, and the Bank of Japan (BoJ) on Friday, September 20. As a result of the former, the British pound against the US dollar reached its highest level in the last 2.5 years. This occurred against the backdrop of the British regulator's decision to keep the key interest rate at the current level of 5.00% and to refrain from hasty measures to reduce it. Consequently, after the announcement of this decision, the GBP/USD pair rose to $1.3339 for the first time since March 2022.

● Despite the decline in UK government bond yields, markets have quickly adjusted their forecasts regarding further easing of monetary policy by the Bank of England (BoE). Currently, according to the median forecast, a rate reduction of 42 basis points is expected by the end of December, compared to the 50 basis points predicted before the last meeting. (Although, it is clear that this adjustment is minor and quite conditional). Macro strategists from the banking group Mizuho International believe that rate cuts will occur slowly, possibly once per quarter. In their view, against this backdrop, GBP/USD has the potential for further growth and could break the 1.3400 level as early as the beginning of October, with the pair reaching $1.4000 by the end of next year, 2025.

Thus, the pound has become the most successful currency among the G10 countries this year. Investors, although expecting a policy easing by the Bank of England in November, are confident that inflationary pressure in the country will remain sufficiently high, supporting relatively elevated interest rates compared to other economies.

USD/JPY: Rate Unchanged, Yen Falls

● Similarly to the Bank of England, the Bank of Japan (BoJ) decided to keep its key interest rate at the same level during its meeting. This decision was anticipated by market participants. However, while the Fed, ECB, and Bank of England are focused on the pace of rate cuts, markets expect the Japanese regulator to do the opposite – raise rates. Nonetheless, BoJ Governor Kazuo Ueda indicated during the press conference following the meeting that he does not plan to accelerate this process. Rates were already increased in March and July of this year, and now it is time to pause and assess the results achieved. Ueda emphasized that the Bank of Japan will continue to raise rates if economic and inflation indicators meet forecasts. However, the weakening of inflationary pressures due to the yen's softness provides the bank with the opportunity to adopt a more cautious approach to future decisions.

● After this statement, the Japanese yen sharply sold off, with the USD/JPY pair reaching a local high of 144.49. Futures on 10-year Japanese government bonds rose by nearly 30 basis points, and the Topix index, reflecting the state of Japan's stock market, showed a 1% increase.

Analysts around the world shared their opinions on the potential consequences of the BoJ's decisions. Experts from Saxo Markets write that “there is no sense of urgency in further normalization from the Bank of Japan. As long as Ueda maintains the same tone, Japanese stocks will enjoy the situation created by the sharp rate cut by the Fed.” In turn, Sumitomo Mitsui Bank believes that the likelihood of rate hikes in December remains low, as the weak yen supports the stock market, which stimulates wage growth.

CRYPTOCURRENCIES: "Bitcoin – the Best Buy in the World"

● Recently, Arthur Hayes, co-founder and former CEO of the crypto exchange BitMEX, compared the consequences of the Fed's interest rate cut for the US economy to the effect of a "sugar high," which can trigger a wave effect and a short-term upward rally. And the rate was cut, immediately by 50 basis points. Risk assets immediately experienced the promised high. The stock indices S&P 500, Dow Jones, and Nasdaq went up, followed by digital assets. To say it was a surge, a jump, or a rally would be an exaggeration. But, according to Hayes, "this is the calm before the storm." "Usually, it goes like this," he writes, "first there is an initial reaction, and the real reaction comes by the close of traditional financial markets on Friday, after which cryptocurrencies follow them—up or down—over the weekend." However, since this review is being written on Friday, we cannot yet verify the accuracy or inaccuracy of BitMEX's co-founder’s words.

● According to Arthur Hayes, the rate cuts amid the growing issuance of US dollars and increased government spending are a mistake for the global financial system but will allow cryptocurrencies to become more sought after by investors, as their yields will rise.

At BlackRock, the world's largest asset management company, it was noted that although it is difficult for investors to analyze cryptocurrencies compared to traditional assets, Bitcoin has nevertheless become a "safe haven" for many amid rising geopolitical tensions. BlackRock strategists note that the leading cryptocurrency could become an effective tool for protection against the ongoing devaluation of the US dollar and global financial risks. Additionally, according to their forecast, as BTC is adopted "as a global monetary alternative," its correlation with US company stocks and dependence on the Fed's rate will gradually decrease.

● Investment strategist and author of the bestseller "Broken Money," Lyn Alden, believes that the adoption of cryptocurrencies in society is not just fast, but rapid. And if Bitcoin remains the leader among digital assets and is considered a reliable store of value, its price in the next ten to eleven years could reach $1 million per coin.

Alden agreed with Ark Invest CEO Cathie Wood's forecast that the price of digital gold could rise to $1.5 million. However, according to the specialist, the timeframes forecasted by Wood are too aggressive. The head of Ark Invest believes that Bitcoin will reach values with six zeros as early as six years from now, by 2030. Alden, however, cites 2035 as the most likely date.

"Not buying bitcoins at this stage would be a crime," declares the author of Broken Money. According to her, "now bitcoin is the best buy on the global market, as this asset has long-term potential." Lyn Alden is confident that in the future, Bitcoin will surpass physical gold. (For reference: the market capitalization of this precious metal currently amounts to about $17 trillion, Bitcoin – $1.17 trillion, that is, 14.5 times less.)

● Let us recall that recently, Jack Dorsey, co-founder and former CEO of Twitter, made a similar statement, suggesting that BTC would reach $1 million by 2030. However, the most impressive forecast was given by MicroStrategy founder Michael Saylor, who stated that Bitcoin will soon increase in price … by 70 (!) times – to $3.85 million. In the long term, according to this billionaire, digital gold could rise to $13 million. However, this is expected to happen only by 2045. By 2050, Bitcoin's market capitalization will amount to 13% of the entire global capital. (For reference: currently, this figure stands at 0.1%).

● Returning from the year 2050 to 2024, let us highlight the forecast of WeRate co-founder Quinten Francois. His data indicate the imminent start of a bull rally. “The average Bitcoin cycle begins approximately 170 days after the halving, and the peak forms after 480 days,” he writes. Based on this, there is not much time left before the rally begins—the surge, according to Quinten Francois's chart, is expected to start on Tuesday, October 8. The analyst also believes that thanks to the Fed's rate decision, there is a possibility that BTC will quickly rise above $64,500. Consequently, during October-November, the coin's price could increase by at least 46%, reaching $90,000-95,000.

● A similar forecast was given by the CIO and founder of MN Trading Consultancy Michael van de Poppe. According to him, the growth of global liquidity will become the key catalyst for the next bull cycle in the digital market. “Cryptocurrencies and commodities are extremely undervalued,” writes van de Poppe, “and it is quite likely that they will enter a 10-year bull market. I expect significant growth from these two asset classes.” According to the expert, the leading cryptocurrency is already ready to rise to $90,000.

As a key support level for Bitcoin, Michael van de Poppe named $58,000. The probability of the price falling below $55,000, according to him, is practically zero. It is worth noting that earlier in September, ARK Invest analysts identified $52,000 and $46,000 as key levels. Meanwhile, the aforementioned Quinten Francois from WeRate believes that it is important for the asset to maintain positions above the critically important zone of $59,000.

● The easing of monetary policy by the Fed and other central banks should also help altcoins. According to analyst Vladimir Cohen, liquidity began to leave this sector in April, which is why fear reigned during the summer. However, the trend has now reversed, and reaching a historical market capitalization peak of $1.1 trillion is just a matter of time. A large amount of liquidity is expected to flow into this market due to the central banks' policy loosening. Furthermore, according to the specialist, some altcoins will demonstrate growth of thousands of percent, while others will ultimately die out. Cohen believes that removing coins that do not offer practical value will play a positive role, as it will make this segment more transparent and liquid.

● Vladimir Cohen also noted that altcoin holders have currently shifted to a long-term holding strategy, ready to endure temporary declines in value while anticipating a future rally. A similar trend is being observed with bitcoin by analysts at CryptoQuant. The available supply of bitcoin is decreasing as users withdraw coins for long-term holding without intending to sell. "Selling pressure is decreasing as fewer coins are available for trading. Some traders are depositing funds into derivative platforms to open long positions, betting on price growth," write the CryptoQuant analysts. However, they also believe that the BTC price is unlikely to undergo significant changes in the short term.

● As of the time of writing, on the evening of Friday, September 20, following the US Fed meeting, the BTC/USD pair moved upwards and is trading around the $62,840 zone. The total cryptocurrency market capitalization has risen slightly to $2.19 trillion (compared to $2.10 trillion a week ago). The Crypto Fear & Greed Index has also increased from 32 to 54 points, moving from the Fear zone into the Neutral zone.

NordFX Analytical Group

Disclaimer: These materials are not an investment recommendation or a guide for working on financial markets and are for informational purposes only. Trading on financial markets is risky and can lead to a complete loss of deposited funds.